Asset Allocation Advice…from a Fortune Cookie

This is an actual message found in my 16-year-old son’s fortune cookie the other day: You will do better in real estate than in stocks. My son said, “Huh? What kind of fortune is that?” And then he asked, “Is that true?”

I snapped a quick pic because I couldn’t believe it either—I mean, really, we get investment advice on the golf course, the pickleball court, at cocktail parties and barbecues…everyone loves a good tip, right? But now we’re getting investment advice from fortune cookies?!

My family is prone to nodding off when I discuss the capital markets, the economy, or portfolio construction, so to summarize my thoughts, I replied to my son’s question, “It depends.”

We face a constant barrage of mixed messaging regarding real estate as an investment. Earlier this week, an article ran in the Wall Street Journal about Blackstone’s bullish $10 billion purchase of AIR Communities, “which owns 76 rental housing communities that are primarily in coastal markets.” And then later in the same week another article in WSJ ran, entitled “The Real Estate Nightmare Unfolding in Downtown St. Louis.” That article addresses the vicious cycle of de-urbanization, characterized by an exodus of commercial, retail and residential activity, followed by tranches of tenants leaving an urban area, no one wishing to be the last tenant stranded in an unpopulated wasteland. And then on the way to the gym this morning, I was reminded by country music artists Jordan Davis and Luke Bryan that “You can’t buy happiness, but you can buy dirt,” which reminded me of what my Nana always said, “Never sell the land.” (I fully realize that not everyone reads the financial press, so therefore “advice” from social media, pop culture and Nana.)

The fuller answer to my son’s question is that real estate plays many roles in wealth, among them being wealth creator, wealth amplifier, wealth detractor, wealth destroyer and wealth diversifier.

Wealth Creator—getting a job, working that job, saving money and buying a house has long been an American formula for wealth creation. The 30-year mortgage is unique to our country, but the credit strategy has indeed created wealth for several generations fortunate enough to buy a home and then pay off that mortgage. Unfortunately, systemic racism in the form of practices such as “redlining” has denied access to this form of wealth creation for scores of minorities and marginalized communities. In more recent years, Federal regulations and economic conditions have had the effect of dramatically tightening mortgage lending while home prices have soared in tandem with borrowing rates. While minorities still face an even steeper climb to home ownership as a residual effect of redlining and other still-present systemic issues, the high cost of home ownership will have a far-reaching effect on wealth creation for younger generations of Americans across race and geographic locations. This role of “wealth creator” for real estate, at least in the traditional residential sense, may be a more limited one for the present, younger generations.

Wealth Amplifier—there is a segment of socio-economic class known as HENRYs, “high earners, not rich yet.” These are typically “young” professionals in the first 10-20 years of their careers who earn well into the six figures or more, may be maxing out contributions to their retirement accounts, usually own a home, enjoy a comfortable—if not sometimes lavish—lifestyle, but who do not have significant liquidity to consider themselves “wealthy.” Within this group, there are those who divert after-tax savings, or who make lifestyle decisions, that afford them the opportunity to buy investment real estate. Typically, these entrepreneurial HENRYs wish to be fully “rich” and are buying single-tenant retail, multifamily properties, or single apartments. The key is that these investors then use the income from their real estate investment and the equity in the property to buy another property, and then another, and then another. The goal, of course, is not only to increase their cash-flow but also build their net worth, which can happen when the strategy is well executed.

Wealth Detractor—I’ve witnessed a dynamic among real estate investors in “wealth amplify” mode who, unfortunately, fail to use debt strategically either by taking on too much or not using an optimal amount. This occurs not only in those relatively new to real estate investing but also among seasoned real estate developers, investors and owner-operators who become over-levered and subsequently doomed to a life on the razor’s edge—the final chapter of which is discussed in the next section.

Wealth Destroyer—MSCI estimates that nearly $820 billion of commercial real estate loans will mature in 2024. Three-quarters of that figure are normally occurring tenors and nearly a quarter, MSCI infers from the data, are loans that were scheduled to have come due in 2023 but received extensions. Both reasons for maturity are relevant: first, in the commercial real estate business, most term loans are 5 – 10 years. As such, loans maturing this year were almost certainly initiated during a period of much lower rates, and borrowers looking to refinance those loans will either be forced to carry a much higher borrowing cost, pay down or pay off the loan, or perhaps even sell the property. Just think back to situation in St. Louis and other urban areas—as leases expired and tenants declined to renew and moved their operations to the suburbs, the owners of the commercial real estate saw a dramatic decrease in their rent rolls and, accordingly, their net operating income. The second reason for the swell of maturities, extensions of previously maturing loans, suggests that the lenders and borrowers were hoping for lower rates as the result of rate cuts this year. However, after this week’s CPI print showing inflation ticking up from the previous month, the Fed will have little reason to cut rates the anticipated three times in 2024, if at all.

All of this paints a bleak picture for any real estate investor who is over-levered while also suffering a decline in rental income. These are the makings of defaults, bankruptcies and, yes, wealth destruction.

Wealth Diversifier—ending on a high note, while real estate investing carries significant risks, the asset can also play a very necessary role in portfolio construction where appropriate. The fortune cookie implied a comparison of real estate to stocks and the suggestion that real estate will always outperform. For all the reasons listed under “detractor” and “destroyer,” we know that real estate does not always outperform, either for the strategy employed in acquiring and maintaining it or due to market and macroeconomic events. That said, there is also an inference in the fortune to which we should pay attention: real estate is not entirely correlated with stocks. One of the key issues with investing today is the over-abundance of beta—which is the degree to which an investment experiences similar volatility to the market as a whole. At higher asset levels, constructing a portfolio that isn’t awash in beta is difficult if not impossible. In the hierarchy of financial planning, once the rainy-day cash fund is fully funded, retirement accounts are on track, and after-tax savings are growing, at a certain point one needs to diversify away from the stock market in order to optimize for long term objectives. Continuing to add more stocks and more bonds to a large portfolio eventually is only adding more of the same…beta.

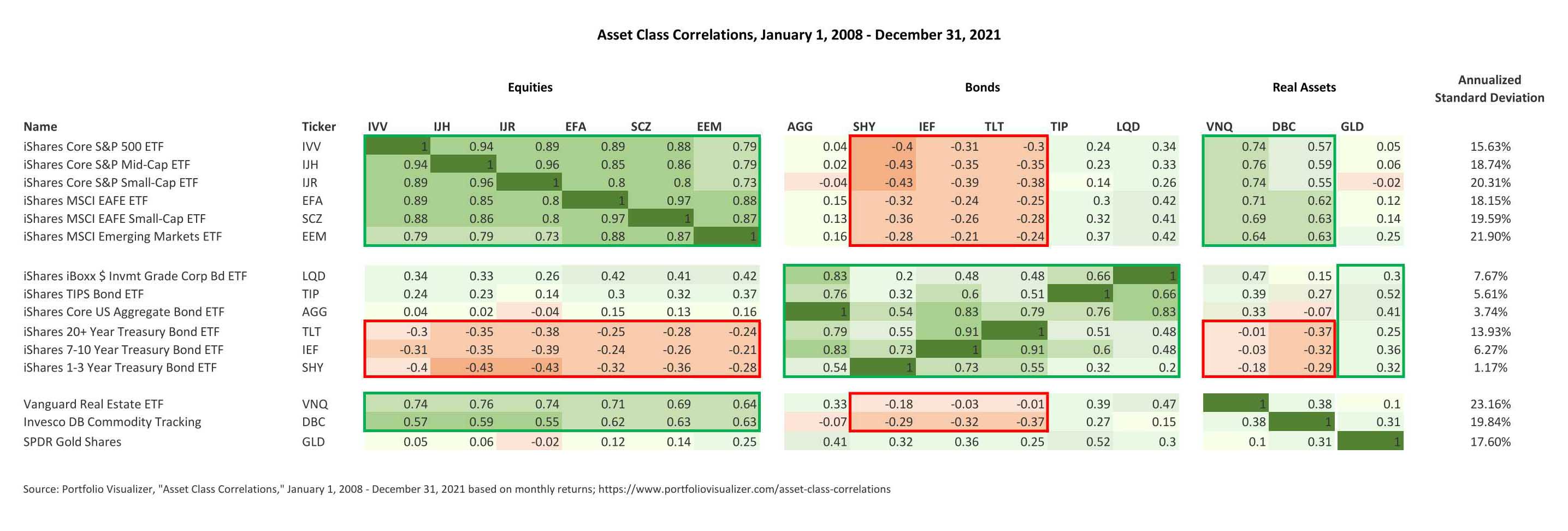

Real estate ETFs and mutual funds tend to carry more beta than private, direct investments in real estate, but even looking at a popular real estate ETF, we see that real estate is less correlated to stocks and is negatively correlated to bonds. Private investments in real estate can be even more lowly correlated to stocks and bonds, can provide a higher income than bond yield or stock dividends, and can produce a healthy total return from appreciation and income.

{kind=link}

Real estate investing carries significant risk of loss, due to interest rate risk, market risk, and, importantly, liquidity risk, among others. Real estate sectors matter, timing matters, investment vehicle matters (i.e. co-mingled funds / pools vs. private, direct investing) and management of carrying costs matters, particularly in the case of operating real estate ventures. Any would-be real estate investors should consult with their financial and tax advisors prior to any investment, because, when unwrapping the question of real estate versus stocks, the first answer is always, “It depends.”